Why digital health is about to enter a “scale game,” leading to more mergers

This is a co-written piece with 7wireVentures’s Alyssa Jaffee

The pandemic was a boom time for digital health. It created massive tailwinds as regulatory barriers were broken down, leading to more innovation than ever before. As the demand for virtual care skyrocketed, entrepreneurs were able to build virtual care companies without needing a physical location present in all 50 states. Enthusiasm for the sector amongst VCs also shot up in the wake a string of impressive exits: Livongo sold to Teladoc for $18.5 billion, and PillPack/ One Medical were acquired by Amazon for around $750 million / $2 billion respectively. Venture capital funding ballooned to more than $29 billion in 2021.

That hype period may have led to many positive developments for the sector, but also some new frictions. Money was flowing out the door so quickly that venture rounds were finalized without much diligence. We saw founders taking millions of dollars off the table in secondaries, and we saw news headline after headline announcing new rounds of capital sometimes a few months after the prior round had closed.

Somehow, amidst all the frenzy, the fundamental first rule of startups was forgotten: Focus on building a great company before all else. VCs investing at the time often found themselves looking at companies that Alyssa likes to call having more “sizzle than steak,” meaning the story was there but not the execution nor the operational excellence.

In the past few years, the market has changed, and there’s no denying it. Good companies are still raising capital, and we’ve seen more examples of that in the past few months. But investors are now far more disciplined on valuations (outside of AI), and on how much they invest. They want to see companies hitting their milestones and finding product/market fit. Because of this, we expect to see companies that struggle to prove a business model finding alternative exit paths or quietly shutting down in 2024 and 2025.

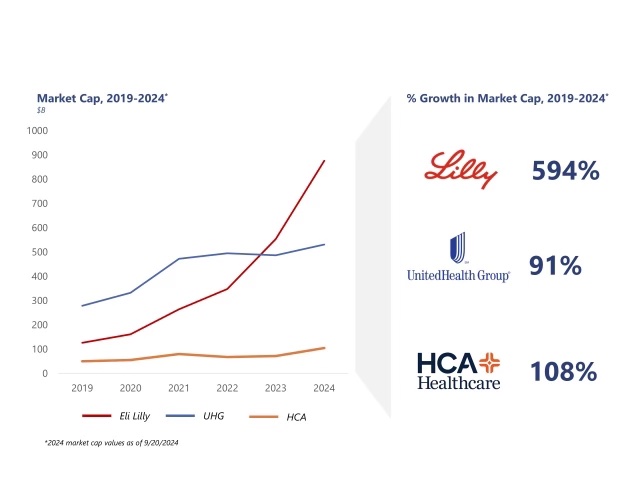

But here’s another trend that hasn’t gotten nearly so much attention. In the time frame that digital health has gone through its own hype cycle – both a boom and a bust – many of health care’s largest incumbents have been on a tear. In the 2020 to 2023 timeframe, as many publicly-traded digital health companies flatlined and struggled, companies like Eli Lily, United HealthGroup (UHG) and HCA continued to grow. To provide a specific example, UHG’s revenue in 2019 was $242 billion, and its market cap was $278 billion. By 2023, its revenue was up $372 billion for the year and its market cap shot up to $487 billion. By the time you’re reading this post, the company’s market cap has hit more than $531 billion!

Meanwhile, UHG’s Optum, announced revenue in 2019 of $113 billion. By 2023, its revenue was up to $227 billion.

So what does this mean for disruptors? Should they simply give up and let the big guys grow even larger?

Well, we’d argue no. But the game does need to be played differently. And to better understand that, we need to take a closer look at an acquisition that occurred in 2020 without a lot of fanfare. That acquisition truly benefited digital health as a sector, but we’d argue it would not have happened in 2024.

In 2024, the rules have been rewritten. So let’s take a walk down memory lane to understand what happened, what we can learn from it, and what’s changed in the years since.

Changing the playbook

Let’s take a look at a deal from four years ago: The $470 million buy-up of AbleTo by Optum.

Optum, which is a unit of UnitedHealth Group (UGH), acquired AbleTo to beef up its virtual behavioral health footprint. At the time, one would have to conservatively estimate that AbleTo was netting somewhere around $50 million in revenue and showing strong momentum. Those numbers were never publicly disclosed, so we can’t know for sure, although we have a hunch that this is about correct.

`