Point Solution fatigue is very real

Thanks to Quantum Health, our sponsor for this piece, for making it free for all subscribers in perpetuity. Quantum Health is a major player in our industry, known for supporting 500 self-insured employers on navigation and care coordination. It reaches 3 million members in the U.S. alone, and uses a mix of human-led experts and proprietary tech to guide employees to the care they need.

The last thing that any health-tech company selling to an employer wants to be labeled is a “Point Solution.”

The term refers to companies that are selling a product or solution targeted to a single condition, such as headaches or diabetes or pregnancy. The theory is that no employer wants to manage dozens of Point Solutions, particularly when it’s unclear if there’s any real return on investment (ROI) in the form of cost savings or improved outcomes for their employees.

Zane Burke, the CEO at Quantum Health sometimes jokes that if all these Point Solutions made good on their promises, then offering employee health benefits would be a “profitable” enterprise, not a cost center. Instead, we’re seeing inflation related to healthcare spending year after year, and employers are drowning in vendors.

Ellen Kelsay, CEO of the Business Group on Health, which represents employers, noted in an interview that the industry has been talking about this issue for at least seven years. There was a time when most employers only had one or two vendor partners; most were “carved in” to a health plan, with a “carve out” for pharmacy benefits and potentially an Employee Assistance Program (EAP) for issues that might impact work performance. Over time, a large number of employers started to think about solutions for employees with chronic conditions, with a goal to serve specific subgroups who may need more help.

After a few years, Kelsay started to feel that the pendulum may have swung too far. The pandemic likely represented the peak, in her view, with large, self-insured employers implementing solutions too hastily to lend a hand during the crisis.

Several experts I spoke to for this piece, including Brian Marcotte, the former executive director of the Business Group on Health and a longtime benefits leader, said they’ve seen some employers balloon to 20 to 30 Point Solutions. It’s not uncommon to be offering half-a-dozen vendors all targeting patients with diabetes or behavioral health.

So where do we go from here?

In a prior post I co-wrote with Big Health co-founder Peter Hames, we discussed crowded the market has become. Because of that, most vendors targeting employers today will have to displace an existing vendor (with a few exceptions, of course). If a condition is known to be a high priority for employers, like oncology, musculoskeletal, or diabetes, chances are that an employer already has one or more vendors in place.

The work going forward will be focused on rationalization and proving ROI. There’s clear risks associated with having too many vendors, going after the same member-base. The last thing we need in health care services is more fragmentation.

Are there exceptions?

Business Group on Health’s (BGH) most recent survey of employers listed a few areas that remain a focus for employers. In those areas, I still see room for vendors, although most are already starting to become saturated.

Here are some of the highlights:

- In the survey, 1 in 2 employers noted that cancer was the number one driver of medical costs and 86% responded that it’s in the top three. The pandemic might well have worsened the crisis, as we know that fewer people were proactive in getting screenings during those years.

- Other top areas driving cost include some of the usual suspects: Musculoskeletal (fairly consistent as a high cost driver for most employers in 2021, 2022 and 2023). About three-quarters of employers describe it as a top three cost driver.

- And Maternity. The first year surveyed, in 2023, it was a top three cost for 23% of employers.

- Interestingly, cardiovascular disease-related costs eclipsed diabetes: 30% of employers described it as a top 3 cost in 2023, versus 27% in diabetes.

- Mental Health was only a top cost for 17% of employers, but the real number could be higher because it’s notoriously difficult to track the true cost. A mental health condition could exacerbate a chronic condition, resulting in an expensive hospitalization, for instance. Mental health, for that reason, is still a top issue though for employers, particularly in the wake of Covid. Where I see the most opportunity for vendors is in tackling more severe conditions, as most are focused on anxiety and depression.

Pharmacy spend also continues to be a focus for employers. Most employers are concerned about high-cost drugs, per the Business Group on Health, and the increase in the median percentage of healthcare dollars spent on pharmacy.

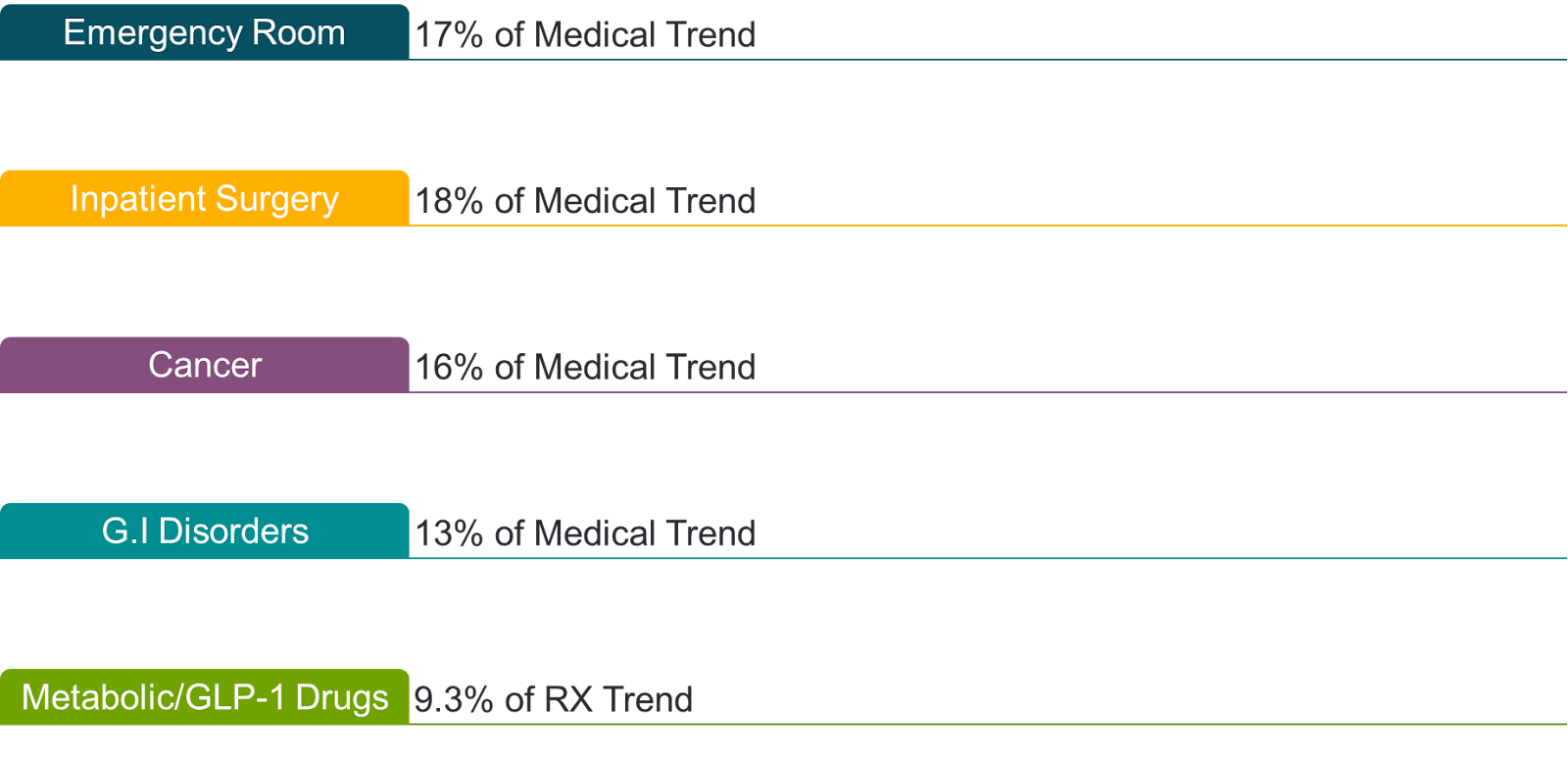

I also received data from Quantum Health, which has its own breakdown of medical “trend and spend.” Per Quantum, this data represents millions of members and is a combination of claims, provider interactions, payers, PBMs as well as information shared via the vendors themselves (see below).

Note: I asked for more granular-level information related to emergency room and inpatient surgery because I was curious what conditions were driving the bulk of the cost. Quantum Health told me for inpatient it was (in order of prevalence): Septicemia, Morbid Obesity, Gallbladder and Biliary disease; Myocardial infarction and Spondylosis/Stenosis. The top drivers of emergency room spending include: Gastro disorders, Eye and ENT disorders, Renal/Urological disorders, followed by trauma and accidents.

Clearly, it’s a top priority for employers to determine how to reduce health care in the wake of rising inflation. In my opinion, that means working with vendors that can reduce those costs by providing high quality care at affordable price points, and it means a lot more transparency from the digital health industry.

Where I see the space evolving:

- More tools and third parties organizations popping up to work with large, self-insured employers to help them curate the various Point Solutions. Groups like Peterson Health Technology Institute have already stepped up to evaluate digital health technologies, and are asking vendors to share data.

- The navigation players, like Quantum Health, Accolade and Included Health, will step up. These companies have access to data-sets that employers can leverage. What’s intriguing to me is where navigators will choose to draw the line. Quantum Health is reluctant to be “king or queen makers,” via Burke. In other words, his company won’t anoint one vendor the “best” in a category; but they will share information with employers based on what they’re seeing and let them make their own decisions.

- We’ll see more efforts to integrate the various digital health vendors to reduce fragmentation.

- I predict we’ll see the rise of more innovative marketing solutions that will help make employees aware of the solutions that their employers are paying for, in the moment that they are looking for help. That’s a dearth of those kinds of offerings today.

In Defense of Point Solutions

If it seems like I’m bearish on Point Solutions, I’m actually not. I think we have too many of them doing the same thing, but I don’t think we should revert back to the status quo. In fact, if you asked me to bet on either a “horizontal” play, like a generic telemedicine platform, or a Point Solution - I’d go with the latter, any day of the week. And if you told me I now have to work with a large payer to figure out maternity care or find a therapist or fix my neck pain, I’d be overwhelmed.

Focusing on one condition at a time forces discipline It is not easy to produce a solution that offers something for everyone. There’s a reason why even in the pandemic, most organizations found that less than 20% of their employees were using a one-size-fits-all telemedicine benefit at all.

The problem with Point Solutions isn’t usually in the care delivery or member experience piece (although that occasionally is actually the problem) - it’s the lack of integration. That includes integration with navigation players - assuming an employer uses one, as well as integration with each other and integration with the system.

This is particularly problematic when the patient doesn’t just have diabetes; they have behavioral health challenges, weight management concerns, a high risk of heart disease and more. What happens to the patient in that case? Are they referred out and the Point Solution loses touch with them from there? And who’s managing that person’s care as a “quarterback” primary care practitioner theoretically should? I fear this happens far too frequently, making it especially challenging for vendors to deliver true ROI.

(As an aside, it seems like a missed opportunity to me that patients who self-select to use a digital service should then get referred into the traditional, brick and mortar health care system, when there’s another great digital option available. Why don’t companies in digital health do more to support each other in the form of warm handoffs and referrals?)

Are investors still backing Point Solutions?

Where does investor sentiment stand today when it comes to point solutions?

I posed the question on “Point Solution fatigue” to an SMS group for female health-tech investors I’ve been involved in for about five years that includes VCs from ACME, Lux and 7wire. Their responses were fairly consistent. Deena Shakir, who co-led Maven Clinic’s Series D, shared that she’d prefer to see “focused excellence,” versus a one-size-fits all solution. Leslie Schrock, an advisor also to Maven, agreed that she’s seen plenty of “verticalized solutions” expand over time into real businesses.

Alyssa Jaffee, in defending Point Solutions, said she and her fellow investors at 7wire have generally these vendors to be more successful in the long-run. “Building a horizontal platform means you’re more things to more people,” she told me. “It requires you to raise a ton of money and doesn’t give you a ton of insights into product/market fit.”

There’s also an interesting trend that I discussed this past month with Liana Douillet Guzman from Folx, which caters to the LGBTQIA+ community and sells its solutions to large employers like Discord, Human Rights Campaign and LiveNation. In her view, the next iteration of Point Solutions is to focus less on the condition and more on the community that a member associates with. Guzman said that Folx can treat its members across fertility and family planning, behavioral health, primary care as well as other forms of treatment, and it has an easier time with both utilization and engagement because its members are so loyal.

“By going narrow for who we care for,” she said, “we go wide in terms of what we can offer them.”

Likewise, Julia Cohen Sebastien, CEO of Grayce, a company that works with an increasing number of employees in today’s workplaces who are caregivers, notes that Point Solutions have gotten a bad rap because they’ve myopically focused on a handful of “high cost areas, some of which are plagued by intractable problems of behavioral economics.” An example there might be chronic condition management, where social factors that play a role are often ignored. Instead, she encourages employers to think about the real problems that “communities” or “sub populations” face, particularly those that can be solved where there’s tangible ROI.

Just like Folx, her company doesn’t just solve for one condition at a time. Grayce has the flexibility to do everything from health care to social care and even managing finances.

I buy into that, particularly as a potential path to solve the member engagement problem. By focusing on what one population needs, and targeting those individuals, there’s an opportunity to provide that broader array of services without straying into “one-sized-fits-all” territory.

The Great Cull

That said, we still need to do something about Point Solution fatigue. It is real.

Quantum Health’s Zane Burke said 9 out of 10 of the company’s employer customers have noted that it’s a problem. “These clients are overloaded… everyday someone is in their ear selling something,” he said. “Once these programs are rolled out, they also don’t know where real ROI is coming from.”

So how do employers decide which vendors to cut without upsetting their employees who may be attached to a particular solution?

One major challenge, according to Centivo’s Gillian Printon, is that whenever something positive happens and it shows up in the data - whether that’s in the form of cost savings or improved health outcomes - then several different vendors will claim credit. Printon, who’s worked with employers for decades, said it’s very hard to track which company is actually responsible, given all the overlap.

Relatedly, vendors are expanding their offerings all the time, particularly as they hear from employer customers and members about adjacencies. As an example, it makes a lot of strategic sense to me as an example that Maven Clinic, which started in pregnancy and postpartum care, should move into menopause. Likewise, Omada Health started out in pre-diabetes, before moving into diabetes, hypertension, and now weight management. Many of the adult behavioral health companies are now moving younger to focus on kids and teens.

What this indicates: Employers and HR departments would rather work with an existing vendor than contract with an entirely new one. For the record, I do see this trend as a positive one - both for Point Solutions to take on more scope and to integrate more closely with each other. But it also creates problems.

There’s also the longstanding challenge around how data is shared between vendors and employers - oftentimes (and understandably) the seller will select the data that paints them in the best possible light. I’d argue that’s where the navigators can play a role, assuming vendors agree to share data. Several employer benefits leaders I spoke to for this piece said they’re struggling with making the right decision, which will continue to be a big priority for 2024/2025.

Where we should go from here

In general, I believe we need to see a lot more transparency in this space, as well as a shift in “pay for outcomes” business models. Employers will increasingly want to pay - and only pay - when a service is being used, and when it’s doing what it claims to do. In my view, per member, per month (PMPM) contracts were a gift to digital health companies, particularly those struggling with utilization. Going forward, companies that are adding real value in the form of cost savings and improved outcomes should be recognized for that, and paid accordingly. That’s what I found interesting about the recent news from Thyme Care, which seemed to accompany its funding announcement: it is moving to a value-based “pay if it works” model. That includes providing incentive payments to physicians and taking a cut of health plan savings.

Gone are the days where a Point Solution with big promises could sell without the goods to back it up. Selling into the employer is more challenging than ever, and it’s going to take something truly special and unique to win.

And some exciting news…!

…Second Opinion is hosting its first-ever dinner for health-tech operators, hosted by yours truly

We need more forums for people to convene who are not the CEO. So we are welcoming ops leaders from the Second Opinion community for an evening to learn from one another, sponsored by Luminai. The goal with this dinner is to create space for real conversations among leaders with shared expertise – think networking and fun, not marketing.

We're hosting our first dinner in NYC September 17 with more details forthcoming. If you're an Ops leader at a Healthcare / Healthtech company and are interested in attending and available on that date, please respond to this email. You can also nominate a co-worker who should attend by filling out this form here. We’ll have 15 spots open. If you’re not in NYC or not available then, fill it out anyways. This is just the beginning!

About the author

Christina Farr

Christina Farr is a healthcare writer and investor. Formerly at CNBC and Reuters, she covers digital health, startups, and policy, blending reporting with analysis and investing perspective to help leaders navigate healthcare’s evolving landscape.

New York City